Buying a Property In Singapore

Frequently Asked Questions to Property Purchase in Singapore

Singapore residential properties are generally classified under 2 broad categories: Private and Public. Private residential properties available for purchase in Singapore include private condominiums, landed properties, strata-titled properties, and are available for sale in both new launch and resale markets. Public housing refers to HDB flats that are subsidised by the government and are reserved for Singapore citizens and permanent residents.

Generally, foreigners are allowed to purchase private residential properties such as condominiums and strata-titled properties in Singapore. They need to seek approval under the Residential Property Act to buy landed properties from the Singapore Land Authority (SLA) Land Dealings Approval Unit (LDAU). Additionally, foreigners are not allowed to buy public housing (HDB flats) unless they are permanent residents or have met certain eligibility conditions (for e.g., buying a resale flat together with a Singaporean spouse) by the Housing & Development Board.

In general, you can borrow up to 75% (Loan-To-Value ratio) of the property value from banks and financial institutions in Singapore. The banks and financial institutions will assess the borrower based on the Total Debt Servicing Ratio (TDSR) framework implemented by the Monetary Authority of Singapore (MAS). The TDSR calculation takes into account all of the borrower's existing debt obligations, such as credit card debt, car loans, personal loans, as well as any existing mortgage loans.

Some of the taxes and fees associated with buying a property in Singapore include the Buyer's Stamp Duty (BSD), Additional Buyer's Stamp Duty (ABSD), legal fees, mortgage stamp duty, agent fees, and valuation fees. The BSD and ABSD rates depend on the property value and the buyer's profile (local/foreigner, 1st/2nd/3rd or more properties owned).

BSD and ABSD rates are subject to change based on government policies. It is important for buyers to consult a licensed property agent or lawyer to understand their tax obligations before buying residential properties in Singapore.

You can approach banks or financial institutions, and provide them with financial documents for assessment. It is important to know what options are available, especially when you need to stretch your loan tenure. At BuyingSingapore, we have an established network of bankers and mortgage brokers to help you find the best loan options, at no additional cost. Rest assured that you will get the best rate from the bank of your choice.

You may engage a licensed valuer to determine the market value of a property in Singapore. At BuyingSingapore, we have access to many bankers, valuers, and valuation platforms to provide market valuations.

The best way to negotiate is to engage the services of a property agent to represent you and negotiate with the seller/seller’s agent on your behalf. At BuyingSingapore, we have access to subscribed transaction data (non-publicly available), and we do comprehensive Comparative Market Analysis (CMA) to ensure you get the best value out of your budget.

You can also research the market prices of similar properties and make a reasonable offer based on the property value.

For a private resale property purchase, upon obtaining the Option to Purchase (OTP), the buyer has typically 2 weeks to exercise the option. Thereafter, it takes between 8-12 weeks to complete the transaction. However, do note that it is possible for the buyer and seller to negotiate on the timelines according to their requirements.

A private new launch (building under construction) purchase is governed by the Controller of Housing. There is a standardised timeline of:

- Initial Payment Schedule (completion within 8 weeks from the Date of Option. If there is any delay, you should submit a request in writing through your lawyer. It is subject to approval.), followed by

- Progressive Payment Schedule

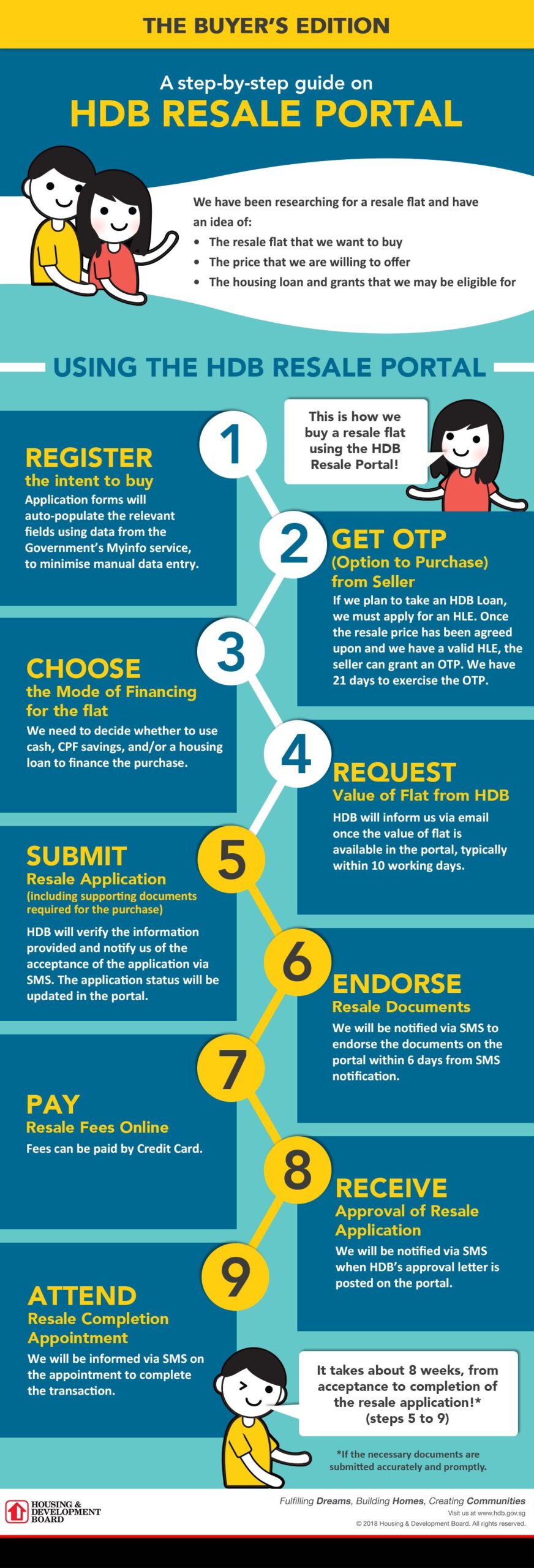

For a resale HDB purchase, the standard Option to Purchase (OTP) exercise period is maximum 3 weeks. Submission period usually takes another 2 weeks. Thereafter, the process follows the attached infographics by HDB.

There are many people who wish to execute both selling + buying transactions concurrently. The timelines for such situations can be complicated, as we need to take into consideration cash and CPF availability. It is best managed by a property professional. At BuyingSingapore, we have the experience in executing complex timelines successfully. Do reach out to us for a property consult before making a property purchase.

We do not charge buyers for assistance with sourcing and purchasing private resale properties or new launch developments. In the case of private resale properties, we will share commissions with the seller's agents. For new launch developments, the developer will pay the commission.

At BuyingSingapore, you will be assigned with one dedicated property consultant to assist you in securing your dream home. Our services include consultation, shortlisting, viewing arrangements, negotiation, and making offers.

For buyers purchasing new launches, BuyingSingapore consultants will use the "7 Steps to Identify Low-Risk and High-Profit Property" investment strategies to help you select a property. This complex process can be completed using our Analyzer mobile application in just a few minutes.

Selling with BuyingSingapore

We charge a standard Buyer Agent Fee of 1% + GST to assist you in finding your dream HDB flat in the resale market. Our comprehensive package includes the following:

- A consultation to determine your preferences for your next home, as well as your timeline and budget (including cash, loan, and CPF usage). We also have a network of bankers from major banks who can offer you the best rates if you require a loan from a private institution.

- We will conduct thorough research using proprietary tools to shortlist the most suitable properties for you. Viewings will then be arranged at your preferred schedule.

- Once you have identified your preferred unit, we will conduct a Comparative Market Analysis (CMA) to determine its market value. This is an important steps to estimate the Cash Over Valuation (COV) if any and provide you with a reference for making an offer. With more than $100 million in transaction value under our belt, we are confident in our ability to negotiate the best price for you.

- We will guide you through the entire HDB submission process, from submission to completion. We can even submit your HDB purchase on your behalf and assist you until you receive your key to your next dream home.

* The information above is updated as of March 2023. As policies may change from time to time, please contact us for the latest updates and how it may affect you. Alternatively, you may also visit the relevant government websites to check on the latest policies details.

* This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your legal, tax, or financial advisors before engaging in any transactions.

You may also like to check out:

→ Buying Consultation details with us

→ Schedule an appointment for a non-obligatory discussion